Polymarket has refused to pay out nearly $11 million in bets on whether the United States would “invade” Venezuela, ruling that the military operation to capture President Nicolas Maduro doesn’t meet the contract’s definition of an invasion—a decision that has sparked fury among traders, revived insider trading concerns, and exposed the fundamental problem with centralized prediction markets deciding their own outcomes.

KEY FACTS AT A GLANCE

- Amount at Stake: $10.5+ million across Venezuela invasion contracts

- Resolution: Polymarket settled as “No” despite U.S. military operation capturing Maduro

- Platform’s Argument: “Snatch-and-extract mission” doesn’t qualify as “military offensive intended to establish control”

- Trader Reaction: Accusations of “bait-and-switch,” calls for class action lawsuit

- Connection: Same suspicious trader who turned $32K into $400K also bet on invasion contract

The Contract Definition Dispute

The controversy centers on a single word: “invasion.” When traders poured over $10 million into Polymarket’s “Will the U.S. invade Venezuela?” contracts, they were betting on whether U.S. military forces would take action against the Maduro regime. On January 3, 2026, U.S. Delta Force operatives captured Maduro at his home in Caracas. President Trump announced the U.S. would “run” Venezuela. To most observers, this looked like the bet had resolved.

Polymarket disagreed.

“This market refers to US military operations intended to establish control. President Trump’s statement that they will ‘run’ Venezuela while referencing ongoing talks with the Venezuelan government does not alone qualify the snatch-and-extract mission to capture Maduro as an invasion.”

— Polymarket official statement

The platform clarified that the contract would only resolve as “Yes” if the U.S. “commences a military offensive intended to establish control over any portion of Venezuela.” A targeted capture operation, Polymarket argued, doesn’t meet that standard—even if it involved 150+ aircraft conducting airstrikes and resulted in the removal of a head of state.

WHAT HAPPENED VS. WHAT POLYMARKET SAYS

What Traders Expected

- 150+ U.S. aircraft conducted airstrikes

- Delta Force captured head of state

- Trump said U.S. will “run” Venezuela

- 32 Cuban military personnel killed

- Head of state now in U.S. custody

Polymarket’s Position

- “Snatch-and-extract” ≠ invasion

- No “military offensive to establish control”

- Diplomatic engagement ongoing

- Contract requires territorial control

- Resolution: NO

The Same Suspicious Wallet Returns

This dispute has an uncomfortable connection to the insider trading scandal we covered last week. The anonymous trader who turned $32,537 into over $400,000 by betting on Maduro’s capture—placing their largest wagers just hours before the operation became public—also placed bets on the invasion contract.

According to NBC News, the same account wagered $1,000 on the U.S. invading Venezuela by January 31, along with $250 on Trump invoking the War Powers Act and $146 on U.S. forces landing in Venezuela. These bets, placed alongside the massive Maduro capture position, suggest the trader expected military action that went beyond a simple extraction.

THE SUSPICIOUS TRADER’S BETS

Maduro out by Jan 31: $32,537 → $436,759 profit (PAID)

U.S. invades Venezuela by Jan 31: $1,000 → $0 (DISPUTED)

Trump invokes War Powers Act: $250 → TBD

U.S. forces land in Venezuela: $146 → TBD

The timing raises an obvious question: If someone had advance knowledge of a military operation significant enough to bet $32,000 on Maduro’s removal, would they also have known whether that operation would qualify as an “invasion” under Polymarket’s definition? Or did even the insider get caught by the platform’s semantic distinction?

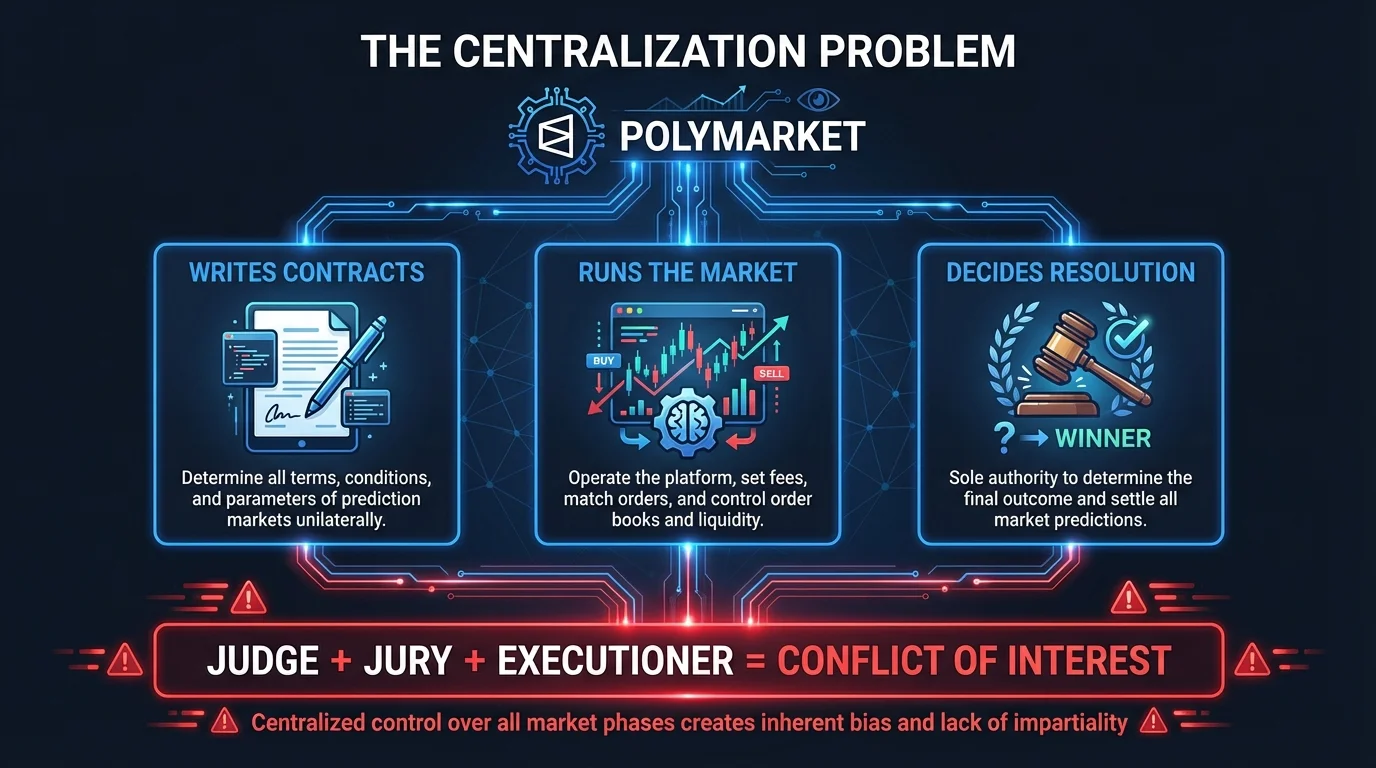

The Centralization Problem

The Venezuela payout dispute exposes a fundamental conflict of interest at the heart of centralized prediction markets. Polymarket isn’t just a neutral venue where traders bet against each other—it’s the entity that writes the contracts, runs the market, and decides the resolution. When $11 million is on the line, that’s a lot of power concentrated in one place.

Traders are calling foul. “Polymarket has descended into sheer arbitrariness. Words are redefined at will, detached from recognized meaning,” wrote one user. Another posted: “Sue Polymarket. Class action lawsuit. Financial fraud.” A third summarized the frustration: “That a military incursion, the kidnapping of a head of state, and the takeover of a country are not classified as an invasion is plainly absurd.”

THE THREE ROLES POLYMARKET CONTROLS

1. CONTRACT CREATION

Polymarket writes the contract language and defines what qualifies as a “Yes” or “No” outcome

2. MARKET OPERATION

Polymarket runs the exchange, matches orders, collects fees, and controls liquidity

3. RESOLUTION AUTHORITY

Polymarket decides how contracts resolve and whether to pay out winning bets

The accusation of “moving the goalposts” is particularly damaging. Traders claim Polymarket added “Additional Context” to the contract terms after the operation occurred—context that narrowed the definition of invasion to exclude what had actually happened. Whether this constitutes fraud or merely aggressive contract interpretation will likely be tested in court.

Why the Torres Bill Matters More Than Ever

The Venezuela payout dispute validates everything Rep. Ritchie Torres warned about when he introduced the Public Integrity in Financial Prediction Markets Act on January 5. That bill focuses on insider trading, but the underlying concern is the same: prediction markets need oversight.

Currently, Polymarket and its rival Kalshi fall under CFTC supervision—an agency with about one-eighth the staff of the SEC, despite prediction markets now handling billions in weekly volume. The CFTC’s insider trading task force, formed only in 2018, has minimal enforcement history and no clear precedent for handling disputes like this one.

REGULATORY GAPS EXPOSED

What’s Missing

- No standard for contract resolution disputes

- No independent arbitration requirement

- No disclosure rules for contract changes

- No recourse mechanism for traders

- Limited CFTC enforcement capacity

What Torres Bill Addresses

- Bans federal officials from insider trading

- Defines material nonpublic information

- Establishes enforcement framework

- Creates precedent for regulation

- Signals Congressional interest in oversight

The complicating factor: Donald Trump Jr. serves as an adviser to both Polymarket and Kalshi. Some experts question whether the CFTC will pursue aggressive enforcement given these relationships. “Given the conflicted relationship of the First Family, CFTC oversight could be compromised,” Yale School of Management professor Jeffrey Sonnenfeld told reporters.

Trust Erosion: The Real Cost

Beyond the $11 million at stake, this dispute threatens something more fundamental: the entire premise of prediction markets as reliable forecasting tools.

The bull case for prediction markets has always been that they aggregate information more efficiently than polls or expert opinion. When real money is on the line, the theory goes, people have incentives to be accurate rather than ideological. Google Finance recently integrated Polymarket data into search results. Mainstream media cite prediction market odds as authoritative forecasts.

But that credibility depends on one thing: trust that winning bets get paid. If Polymarket can refuse payouts by arguing that capturing a head of state and announcing plans to “run” his country doesn’t constitute an “invasion,” why would anyone risk serious money on political outcomes?

“That a military incursion, the kidnapping of a head of state, and the takeover of a country are not classified as an invasion is plainly absurd.”

— Polymarket trader

The invasion contract now trades at just 4% odds of resolving “Yes” by January 31—down from much higher levels before Polymarket announced its interpretation. Traders who bought at higher prices, believing they’d won, are now looking at near-total losses unless they can mount a successful legal challenge.

The Pattern Emerges

Connecting the threads across our Venezuela coverage reveals a troubling pattern:

JANUARY 3: THE CAPTURE

U.S. forces capture Maduro. Suspicious trader’s $32K bet pays $400K+. Three wallets profit $630K total.

JANUARY 5: THE RESPONSE

Rep. Torres introduces insider trading bill. Public Integrity in Financial Prediction Markets Act targets federal officials.

JANUARY 7: THE REFUSAL

Polymarket refuses to pay $10.5M in invasion bets. Traders accuse platform of changing contract terms after the fact.

The same suspicious trader who profited from apparent insider knowledge about the capture is also exposed to the invasion contract dispute. The same regulatory gaps that enabled potential insider trading also enable platforms to unilaterally refuse payouts. The same oversight vacuum that Rep. Torres is trying to address is the same one that leaves traders with no recourse when platforms redefine terms.

Prediction markets promised to be the future of information discovery—decentralized, transparent, and incorruptible. The Venezuela saga suggests they may have inherited all the problems of traditional finance while adding new ones: centralized resolution power, regulatory arbitrage, and the ability to profit from classified information with minimal enforcement risk.

KEY TAKEAWAYS

- $10.5M in dispute — Polymarket refuses to pay invasion bets despite U.S. military operation capturing Maduro and Trump announcing plans to “run” Venezuela

- Contract definition is everything — The dispute hinges on whether a “snatch-and-extract mission” constitutes an “invasion intended to establish control”

- Same suspicious trader — The account that turned $32K into $400K on Maduro’s capture also bet on the invasion contract

- Centralization problem — Polymarket writes contracts, runs the market, and decides resolution—judge, jury, and executioner

- Torres bill gains relevance — The dispute shows why prediction markets need regulatory oversight beyond what CFTC currently provides

- Trust at stake — If platforms can refuse payouts on technicalities, the entire prediction market thesis is undermined