A 19-year-old in California can’t legally bet $10 on the Lakers at DraftKings. But she can legally trade a $10,000 position on the Super Bowl at Kalshi—a CFTC-regulated exchange that’s seen $5.8 billion in monthly volume, 90% of it from sports contracts. The difference? A three-year age gap in federal versus state law that has transformed college campuses into the primary liquidity engine for America’s fastest-growing financial market.

KEY FACTS AT A GLANCE

- The Loophole: Kalshi requires 18+ (CFTC-regulated); DraftKings/FanDuel require 21+ (state-regulated)

- Market Volume: $5.8 billion monthly on Kalshi (November 2025), 90% from sports

- Geographic Arbitrage: Kalshi legal in California, Texas, Utah—where sports betting is banned

- Average Fees: Kalshi ~1.2% per contract vs. DraftKings ~4.5% juice

- NCAA Position: Calls prediction markets “catastrophic threat” to college sports integrity

The Three-Year Loophole

The regulatory architecture that created this market is elegantly simple: state gaming commissions regulate sportsbooks and universally impose 21+ age limits (with exceptions in Kentucky, New Hampshire, Wyoming, and Washington D.C.). The Commodity Futures Trading Commission regulates Kalshi as a “designated contract market” trading “event contracts”—not bets. Under federal law, the minimum age to trade derivatives is 18.

This creates a massive addressable market. Freshmen, sophomores, and juniors aged 18-20 are legally barred from DraftKings but can freely trade NFL outcomes on Kalshi. The platform operates federally, making it legal in California, Texas, and Utah—states where online sports betting remains banned. For millions of college students, Kalshi isn’t an alternative to legal sportsbooks. It’s the only legal game in town.

Following Kalshi’s 2024 legal victory against the CFTC—where courts ruled the agency couldn’t arbitrarily ban contracts simply because they involved events people also gamble on—the dam broke. The distinction between “gaming” and “event contracts” narrowed to the point of irrelevance for end users. A student trading “Kansas City Chiefs to win” on Kalshi is functionally making a sports bet, but legally making a derivatives trade.

How Students Actually Get Started: The Kalshi Onboarding Process

Creating a Kalshi account is designed to feel like opening a brokerage account, not joining a sportsbook. The requirements and process reveal how the platform positions itself within the regulatory framework.

KALSHI REQUIREMENTS

- Age: 18+ (the key differentiator from 21+ sportsbooks)

- Residency: Legal U.S. residential address (50 states, D.C., or territories)

- Identity: Valid SSN and government-issued ID (passport or driver’s license)

Step-by-Step Process:

Go to Kalshi.com and click “Sign Up”—email, Google, or Apple account

Enter phone number, address, and date of birth

Provide last four digits of Social Security Number

Identity verified through Verify.com (automated)—typically approved within 48 hours

Debit card (instant, $2,500/day cap), bank transfer (2-4 days, $10,000 daily), crypto (USDC, BTC, SOL, WLD), or wire

Sign-up Bonus: $10 with referral code after placing $100 in trades within 30-90 days (varies by promo). Note: Promo availability is restricted in Arizona, Illinois, Maryland, Michigan, Montana, Nevada, New Jersey, and Ohio.

KEY FRICTION POINT FOR STUDENTS

The SSN requirement creates a barrier. Many college students—especially international students—may not have one readily available or may be hesitant to provide it. Unlike sportsbook apps that verify identity through state gaming databases, Kalshi runs full financial KYC checks more akin to opening a brokerage account.

Kalshi vs. DraftKings: Complete Comparison

Understanding the practical differences between these platforms goes beyond the age requirement. Here’s how they stack up for students deciding where to place their money. Tools like an odds converter can help translate between Kalshi’s contract prices and traditional betting odds.

Fee Structure Deep Dive

Kalshi uses a variable fee structure based on contract price. Taker fees (market orders) are calculated as: Fee = roundup(0.07 × Contracts × Price × (1 - Price)). Maker fees for resting orders are 75% lower.

Compare this to DraftKings’ standard vig on spreads and totals: -110 on both sides equals 4.54% juice. That means you need to win 52.38% of bets just to break even. On a 50/50 spread bet, Kalshi’s ~1.75% fee beats the sportsbook’s ~4.54% vig.

The catch: Research shows Kalshi contracts exhibit “favorite-longshot bias”—contracts with low prices (longshots) win less than required to break even, while high-priced contracts (favorites) perform better. Factoring in fees, the average return across all contracts is reportedly minus 22%. The actual effective cost depends heavily on what you’re trading.

Other Kalshi Fees: Deposits are free (ACH, wire, crypto). Withdrawals cost $2 flat via debit card but are free via bank transfer. Uniquely, Kalshi pays 3.75-4% APY interest on your balance—including funds tied up in open positions.

State-by-State Availability: The Loophole States

This is where the 18+ loophole becomes most relevant. In states where sports betting is illegal or heavily restricted, Kalshi provides the only legal avenue for young adults to bet on games.

States Where Kalshi Has Faced Legal Challenges: Nevada, New Jersey (Kalshi won in federal court in both), Maryland (lost preliminary injunction), Massachusetts (AG sued in September 2025), Illinois (IGB cease and desist in April 2025), and Connecticut (investigation launched April 2025). The coming jurisdictional battles will determine the loophole’s future.

The Financial Nihilism Driver

The behavior of the “student trader” isn’t irrational—it’s a calculated response to perceived economic foreclosure. The sociological concept driving campus adoption is “financial nihilism”: the belief that the traditional social contract—thrift, diversified savings, long-term compounding leading to asset ownership—has fundamentally broken down.

Facing a housing market where ownership rates are projected to be significantly lower than previous generations, and burdened by stagnating wages relative to inflation, the rationale for conservative financial behavior has eroded. The response is a shift toward high-variance strategies. When “slow and steady” feels futile, binary outcomes that resolve in hours become rationally appealing.

Prediction markets align perfectly with this psychology. Unlike equities (slow compounding) or savings accounts (negative real returns during inflation), event contracts offer 100-200% returns in days. World Economic Forum research indicates Generation Z prioritizes usability, technological sophistication, and direct participation over institutional advice. Prediction markets—particularly blockchain-based platforms like Polymarket—market themselves as “trustless” and “transparent,” appealing directly to a generation that doesn’t distrust finance itself, but distrusts the access provided by traditional gatekeepers.

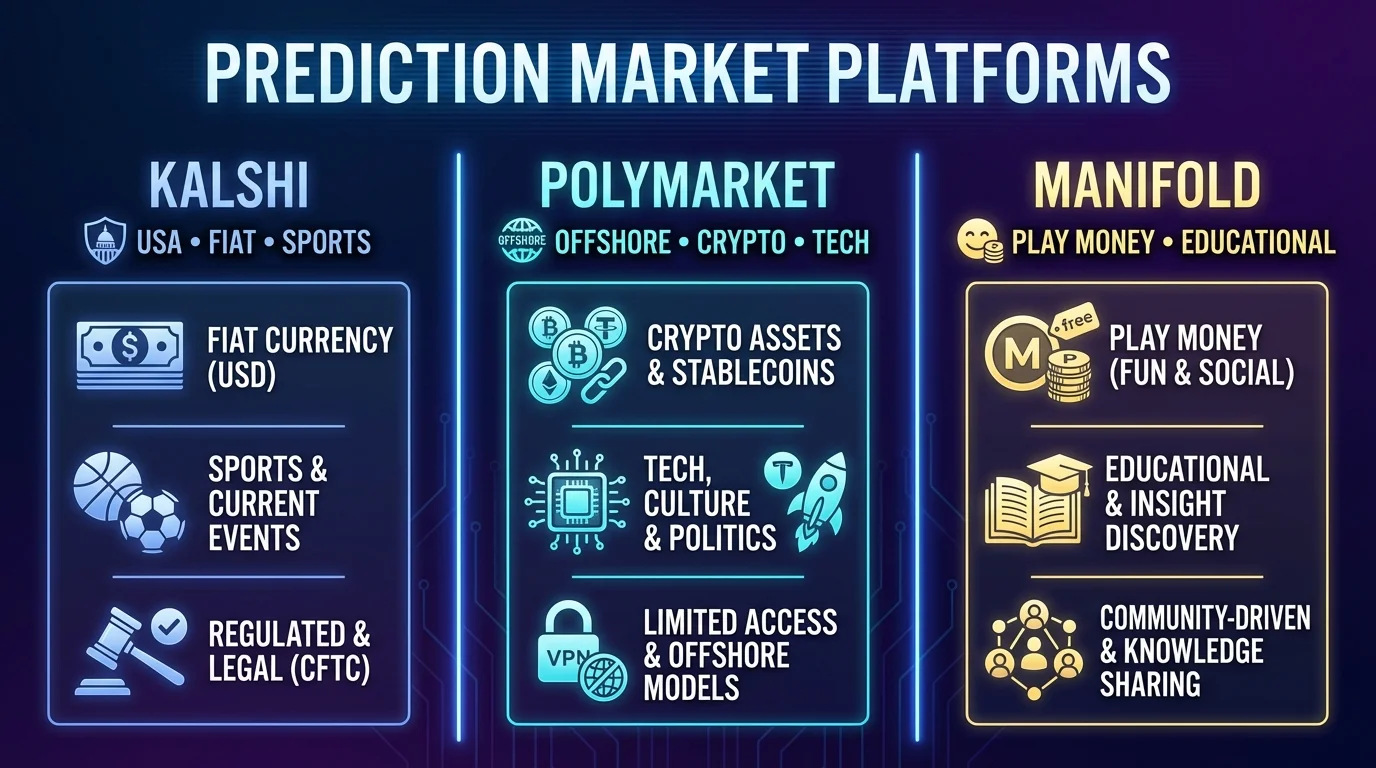

Platform Segmentation: Three Markets, Three Demographics

The student market isn’t monolithic. Three platforms have carved distinct niches based on regulatory status, technical barriers, and cultural alignment.

Kalshi captures the general undergraduate population—sports fans who want to bet on games legally before they turn 21. The interface is indistinguishable from a sportsbook. Polymarket attracts computer science and engineering students at schools like MIT, Stanford, and Waterloo—crypto-natives who view the blockchain-based platform as programmable infrastructure, not just a betting venue. Manifold serves the “rationalist” and Effective Altruism communities at elite universities, offering play-money tiers that professors use in classrooms without legal risk.

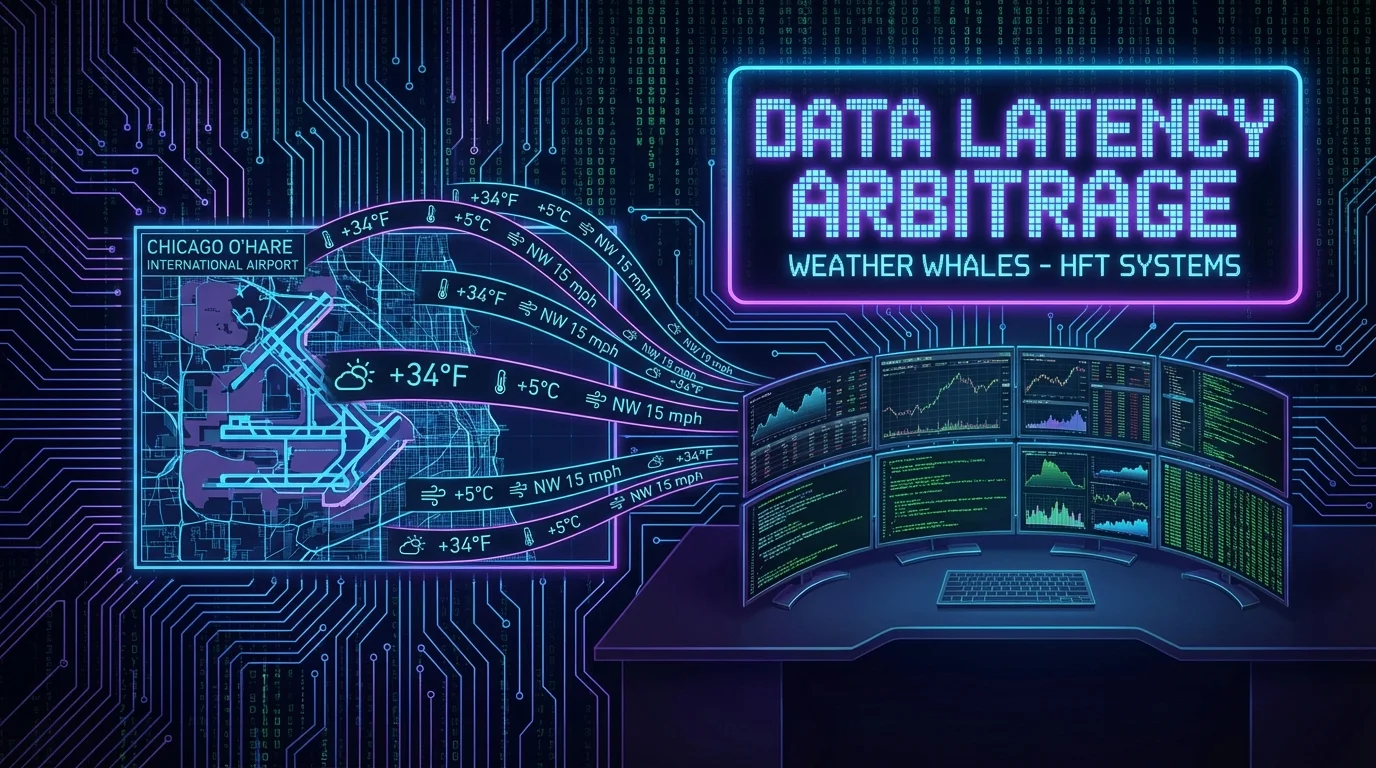

The Weather Whales: A Big Ten Case Study

The most striking example of “campus alpha” emerged from a Big Ten university’s computer science department. According to Kalshi’s official blog (November 2025), two students named Eric and Jerry rented office space on campus to trade Kalshi’s weather markets full-time.

Both students had interned at top trading firms before putting their Computer Science and Computer Engineering degrees to work on Kalshi. They started in February 2024, with Eric initially losing $1,000 before taking a break and returning in September 2024. Their approach was methodical: primarily acting as market makers rather than taking directional bets.

“We think we have one of the best systems among Kalshi traders. It allows us to scale into a lot of different markets with fairly high volume. With our meticulously designed execution strategies, we can implement trades you couldn’t do just by clicking on the platform.”

— Eric, Big Ten student trader

Their edge wasn’t front-running data feeds as initially reported—it was algorithmic market-making and execution. Weather contracts present unique challenges: “The temperature can vary even a couple of meters apart; different sensors can give different readings. To get the actual number took a lot of work for us to price it well.” Initial capital turned into a 100x return. Smart bankroll management was likely key to sustaining their operation through early losses.

This case illustrates the “campus alpha” thesis: technical aptitude, free time, localized data access, and tolerance for risk combine to exploit market inefficiencies that institutional traders ignore. The university environment provides everything needed—high-density information networks, technical talent, and actors with nothing to lose.

Campus Recruitment and Academic Legitimacy

Kalshi has aggressively targeted the collegiate demographic. In 2025, the company launched a “Kalshi Ambassadors Program” explicitly designed to “bring the next 100M users to prediction markets,” identifying college campuses as the breeding ground. The program was later removed from the web following regulatory and public backlash—but its existence reveals the strategic reliance on students as a growth engine.

Polymarket has taken a different approach: hackathon sponsorship. Events like “NexHacks” ($1M prize pool) feature Polymarket as a top-tier sponsor, offering bounties for students who build tools on their protocol. At the Midwest Blockchain conference, Polymarket offered $5,000 specifically for prediction market tooling. This crowdsources R&D to university students for the cost of a few thousand dollars in prizes.

The academic world has provided legitimacy. Professor Rajiv Sethi at Barnard College incorporated live prediction market analysis into his “Introduction to Economic Reasoning” course, having students analyze divergence between statistical polls and market prices during the 2024 election. The University of Pennsylvania has published research showing prediction markets often outperform expert forecasters. This academic seal of approval reframes trading from “gambling” to “applied information theory”—lowering psychological barriers for students who might otherwise hesitate.

NCAA vs. CFTC: The Coming War

The National Collegiate Athletic Association has identified prediction markets as a “catastrophic threat” to college sports integrity. NCAA President Charlie Baker has engaged in an aggressive public campaign urging the CFTC to suspend all college sports markets.

The specific flashpoint was Kalshi’s attempt to list contracts on which athletes would enter the “transfer portal” (the system for college athletes changing schools). The NCAA argued this would incentivize “insider trading” on campuses—a student in a dorm with a football player might know about a transfer decision before the public, creating financial incentives to exploit that relationship or harass the athlete for information. Under pressure, Kalshi shelved those contracts, but broader college game markets remain active.

The NCAA’s deeper concern is “prop bets”—proposition contracts on individual player performance (“Will Quarterback X throw for 300 yards?”). Unlike professional athletes, college athletes are often unpaid (or paid via variable NIL deals) and embedded in the general student population, making them accessible targets for coercion or collusion by student traders looking to engineer specific outcomes.

THE REGULATORY STANDOFF

State attorneys general have begun filing lawsuits against Kalshi. The company’s 2024 legal victory established that the CFTC can’t arbitrarily ban contracts—but it didn’t settle whether states can regulate these platforms under their own gaming laws. The coming jurisdictional battle will determine whether the 18+ loophole survives.

The Responsible Gambling Gap

One of the most significant differences between Kalshi and traditional sportsbooks isn’t the age limit—it’s the consumer protection infrastructure.

In March 2025, Kalshi launched a “Consumer Protection Hub” with voluntary opt-out, trading breaks, and personalized funding caps. But the Massachusetts Attorney General’s complaint alleges Kalshi “consistently fails to provide compliant self-limiting options to Massachusetts bettors, such as appropriate maximum deposits or maximum wagers.”

The regulatory gap is fundamental: CFTC rules do not require platforms to offer traditional responsible-gambling tools such as self-exclusion, loss limits, or compulsory time-outs. This is a significant gap that regulators and public health advocates have flagged—particularly given the platform’s appeal to young adults.

Tax Implications: The 2026 Wrinkle

A provision in the One Big Beautiful Bill Act, signed by President Trump on July 4, 2025, caps gambling loss deductions at 90% starting January 1, 2026. For traditional sports bettors, this creates a scenario where you can break even on the year and still owe taxes.

The uncertainty for Kalshi traders is unresolved. Because Kalshi operates as a CFTC-regulated exchange, some argue trades should be treated like financial instruments (where 100% of losses offset gains under different tax rules). But the IRS hasn’t clarified this. Students using Kalshi should consult a tax professional—the treatment of prediction market gains may differ from both traditional gambling income and securities trading.

The Liquidity Fingerprint

Trading data reveals patterns consistent with novice, retail-heavy participation. Analysis of Polymarket and Kalshi liquidity shows “ultra-short-term” markets (single drives in football games, rapid geopolitical events) see disproportionately high volume—63% of these markets see zero trading after the initial burst, indicating “hit and run” speculation rather than position management.

Academic research on Kalshi pricing reveals a systematic “favorite-longshot bias”: low-probability bets are consistently overpriced. Traders willingly pay premiums for small chances at huge payouts—buying contracts at 2 cents hoping for $1. This is the signature of recreational traders seeking lottery-ticket returns, not institutional hedgers who would arbitrage away such inefficiencies.

The implication is clear: prediction markets’ liquidity is increasingly supplied by young, risk-tolerant traders seeking high-variance outcomes—exactly the profile of a college student applying “financial nihilism” to the markets.

KEY TAKEAWAYS

- The 18 vs 21 loophole is the engine — Federal regulation at 18+ while state sportsbooks require 21+ creates millions of legal users locked out of DraftKings but welcomed on Kalshi

- $5.8 billion monthly volume, 90% sports — Despite being founded for economic hedging, Kalshi’s user base has decisively pivoted the platform toward sports betting

- Cheaper than sportsbooks, more expensive than crypto — Kalshi’s ~1.2% average fee beats DraftKings’ 4.5% vig but costs 100x more than Polymarket’s 0.01%

- Available where sportsbooks aren’t — California, Texas, and eight other major states have no legal sports betting but allow Kalshi

- Responsible gambling tools lag behind — Unlike licensed sportsbooks, Kalshi isn’t required to provide loss limits, session alerts, or mandatory self-exclusion

- The Weather Whales prove the thesis — Big Ten students using algorithmic market-making for 100x returns demonstrates how campuses have become trading infrastructure

- Tax treatment remains uncertain — The IRS hasn’t clarified whether Kalshi gains are gambling income or derivatives trading, with significant implications under 2026 tax rules

- State lawsuits loom — The CFTC loss established federal permission, but states may yet regulate these platforms under their own gaming laws

Sources

- CFTC Designated Contract Markets — CFTC.gov

- Kalshi Regulatory Status — Kalshi.com

- Big Ten Student Traders Interview — Kalshi News, November 2025

- Polymarket — Polymarket.com

- NCAA Statements on Sports Betting — NCAA.org